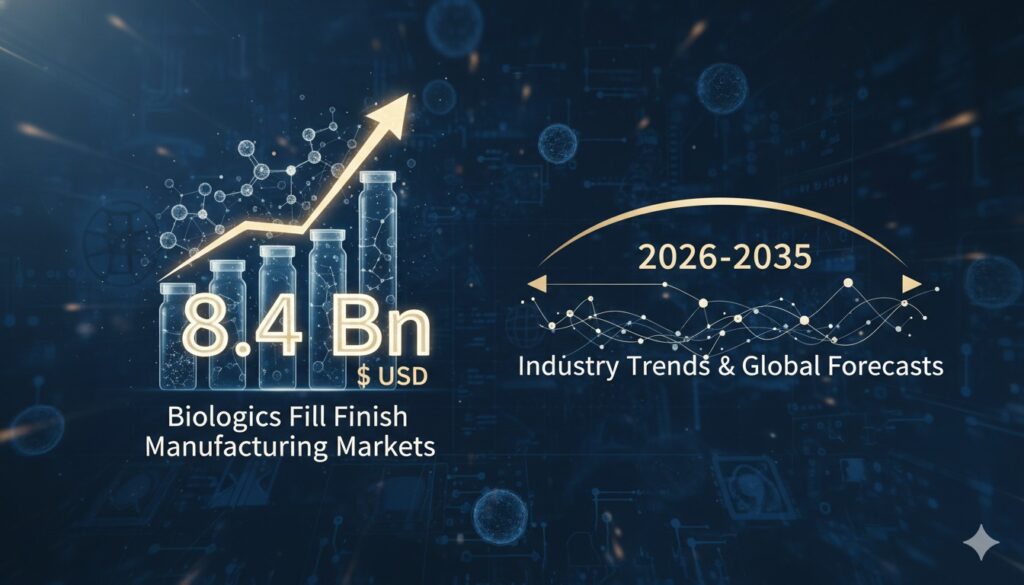

The biologics fill-finish manufacturing sector is set for steady expansion, driven by surging demand for injectable biologics to treat chronic and complex diseases. The market is projected to nearly double from approximately $4.7 billion in 2026 to $8.4 billion by 2035, reflecting a compound annual growth rate of around 6.7%. Key segments include vials and prefilled syringes as dominant packaging formats, with antibodies and recombinant proteins leading biologic types. Outsourcing to contract manufacturers continues to rise amid capacity constraints, while advancements in aseptic technologies and automation support scalability for commercial operations, particularly in oncology, autoimmune, and metabolic disorders.

Biologics Fill-Finish Manufacturing: A Critical Link in the Biopharma Supply Chain

The fill-finish stage represents one of the final and most sensitive steps in biologics production, where formulated drug substances are aseptically filled into primary containers such as vials, prefilled syringes, cartridges, or ampoules, then sealed, inspected, and prepared for distribution. This process demands stringent sterility controls to prevent contamination, given the sensitivity of biologics to environmental factors, heat, and particulates. As the biopharmaceutical industry shifts toward more complex modalities—including monoclonal antibodies, recombinant proteins, vaccines, cell therapies, gene therapies, and nucleic acid-based products—the fill-finish requirements have evolved to accommodate higher viscosities, smaller batch sizes for personalized medicines, and enhanced containment for potent compounds.

The market’s trajectory reflects broader trends in biologics adoption. Chronic conditions such as cancer, autoimmune diseases, diabetes, and cardiovascular disorders continue to drive demand for targeted therapies, many of which require parenteral administration. This has led to a proliferation of biologic candidates entering clinical and commercial stages, placing pressure on manufacturing infrastructure. In-house capabilities at many biopharma companies remain limited for fill-finish, particularly for high-throughput commercial scales, prompting increased reliance on specialized contract service providers.

Capacity constraints have been a persistent challenge. Many drug developers face bottlenecks in scaling up sterile filling lines, especially for novel modalities like cell and gene therapies that often involve low-volume, high-value batches. Outsourcing has emerged as a strategic solution, allowing companies to access flexible capacity, advanced automation, and regulatory-compliant facilities without heavy capital investment. Contract manufacturing organizations (CMOs) now handle a significant portion of fill-finish activities, offering end-to-end services from formulation support to final packaging.

Technological advancements are reshaping the landscape. Automation and robotics have improved precision, reduced human intervention, and minimized contamination risks in aseptic environments. Single-use systems are gaining traction for their flexibility and lower cross-contamination potential, particularly in multi-product facilities. Isolator technology and restricted access barrier systems (RABS) enhance sterility assurance levels, while real-time monitoring and advanced inspection tools ensure product quality. These innovations support faster turnaround times and compliance with evolving regulatory standards from agencies focused on patient safety and supply chain resilience.

Segmentation highlights distinct growth patterns across categories. By primary packaging container, vials remain widely used for lyophilized products and stability needs, while prefilled syringes offer convenience for self-administration and have seen rapid uptake in chronic disease treatments. Cartridges support pen injectors and auto-injectors, and ampoules serve niche applications requiring high barrier properties.

In terms of biologic type, antibodies dominate due to their versatility in oncology and immunology, followed by recombinant proteins for metabolic and endocrine disorders. Vaccines contribute through periodic surges in public health initiatives, while emerging areas like cell therapies and gene therapies present specialized demands, often requiring cryogenic handling or closed-system processing.

Scale of operation divides the market into preclinical/clinical and commercial segments. Commercial-scale activities account for the majority of revenue, as successful approvals transition products to large-volume production. Therapeutic areas show oncology leading, given the high number of biologic approvals in cancer immunotherapy, followed by autoimmune disorders, infectious diseases, metabolic conditions, and others.

End-user dynamics underscore the outsourcing trend. Pharmaceutical and biopharmaceutical companies increasingly partner with CMOs to mitigate risks and accelerate time-to-market. Company size influences preferences, with large firms leveraging integrated networks and mid-sized or small players focusing on niche expertise.

Regionally, North America and Europe hold commanding positions, benefiting from established biopharma hubs, robust regulatory frameworks, and high R&D investment. Asia Pacific is emerging as a high-growth area, driven by expanding manufacturing capabilities, cost advantages, and rising domestic demand for biologics.

The competitive environment features a mix of global CDMOs with extensive fill-finish networks and specialized providers focused on advanced therapies. Investments in facility expansions, technology upgrades, and strategic acquisitions continue to intensify as players position themselves for sustained demand growth.

Key market drivers include the expanding biologics pipeline, regulatory emphasis on aseptic processing excellence, and the push toward patient-centric delivery formats. Challenges persist around supply chain vulnerabilities, skilled labor shortages, and the high costs of maintaining compliant facilities.

Overall, the biologics fill-finish manufacturing market stands poised for measured but consistent growth through 2035, underpinned by innovation and the indispensable role of sterile filling in delivering safe, effective biologic therapies.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or medical advice. Market projections are based on industry analyses and may be subject to change due to economic, regulatory, or technological developments.